Step 01

Initial structure

The starting point is documented before any legal or tax step is planned.

Diagrams

Visuals help make tax structures explainable. The diagrams are anonymised model graphics and review paths, not client references. They are intended to support orientation before a detailed review.

The map shows how relocation, foundations, holding structures, substance, banking, valuation and documentation interact.

A compact map of the main workstreams: persons, entities, assets, jurisdictions, taxes, banking and implementation.

Foundation and business ownership layers shown as a review model.

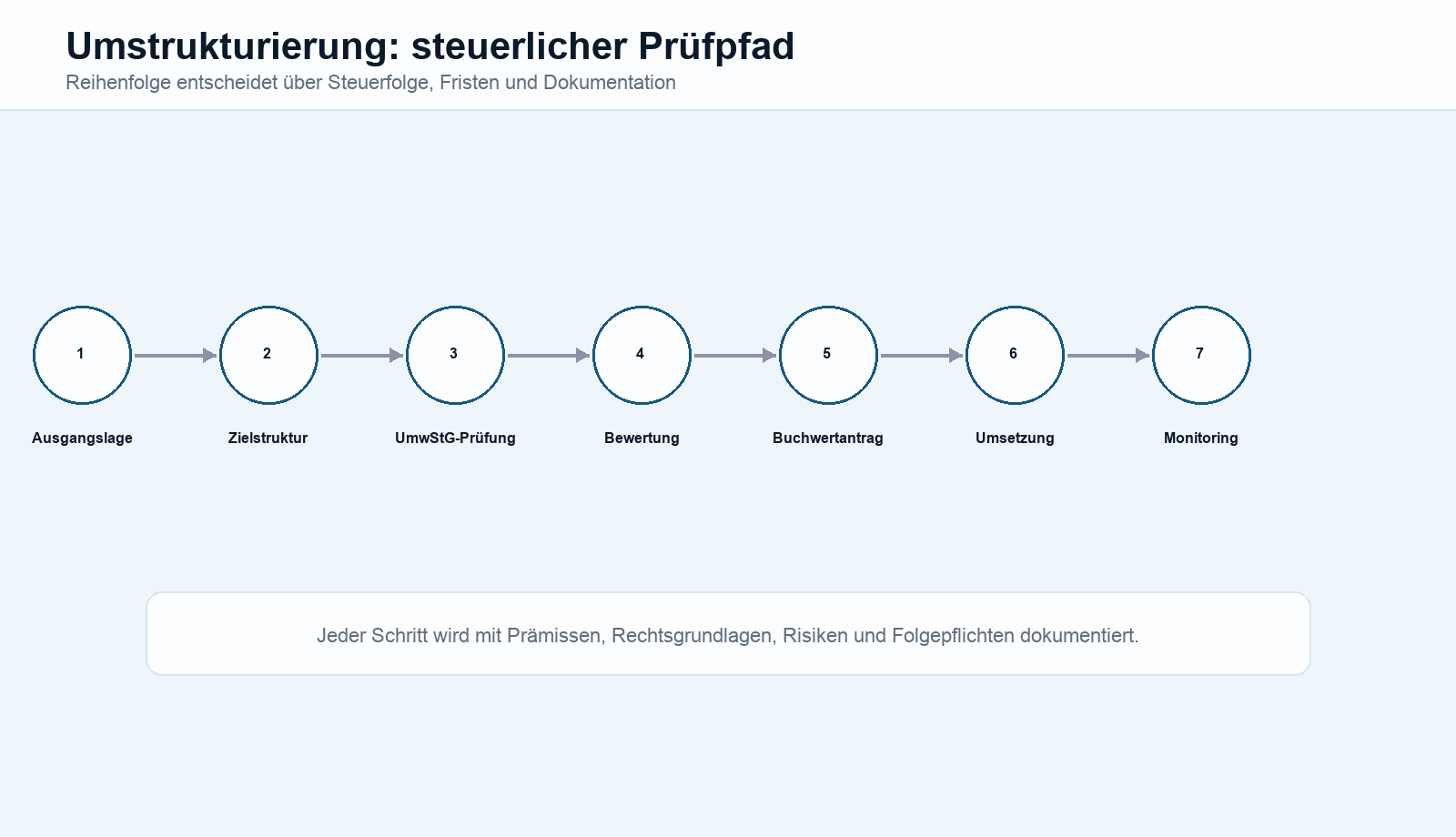

Sequence, valuation, lock-up periods and documentation before implementation.

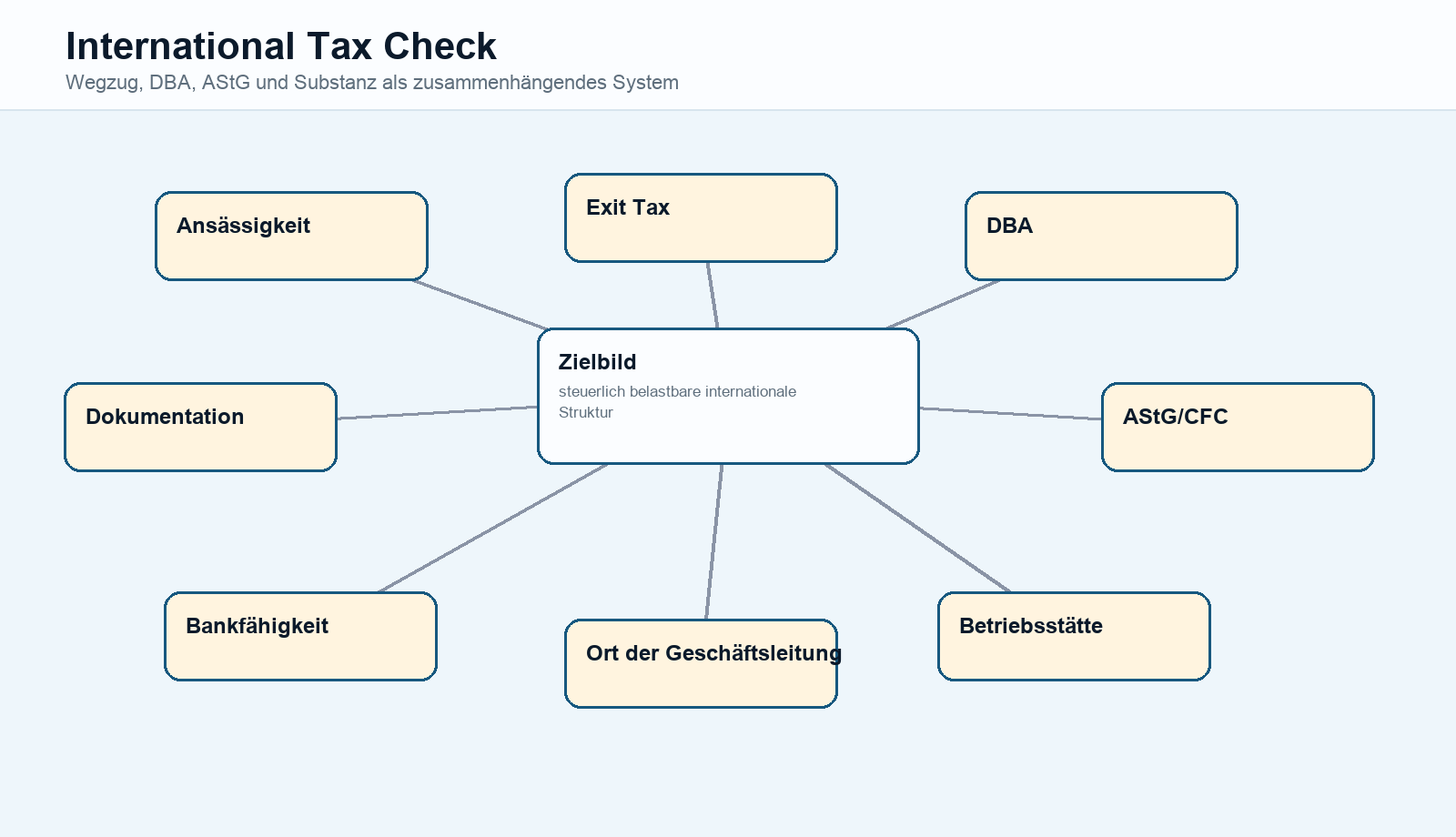

Residence, effective management, permanent establishment, CFC rules, treaties and withholding tax.

Business assets, administrative assets, valuation and relief are organised as a review path.

Purpose, asset dedication, use of funds and ongoing conduct in a foundation context.

Relocation and functional transfers must be reviewed before assets or people move.

Asset protection is shown as governance and ownership order, not as a promise of shielding.

Company, foundation, partnership and holding layers are compared by role.

The following model visuals break down a foundation-holding development path into stages.

The starting point is documented before any legal or tax step is planned.

The holding layer is reviewed for contribution, lock-up periods and distributions.

The partnership layer is assessed for functional allocation and future relocation questions.

The foundation layer is reviewed for ownership, governance and beneficiary logic.

The target picture combines tax, banking and governance explanations.